Sacha Jingree

Periods of heightened market volatility are traditionally when investors turn to so-called “safe havens” to help protect portfolios. Assets such as gold, the US dollar, and US Treasuries are often assumed to provide stability when geopolitical, economic, or financial risks rise. Yet recent market behaviour suggests that these assumptions may not hold consistently across different market conditions.

What is a safe haven, and how is it different from a safe asset?

A safe haven is typically understood as an asset expected to retain value, or potentially appreciate, during periods of acute market stress. It is often sought for short-term protection when risk sentiment deteriorates.

A safe asset, by contrast, is generally held over the medium to long term to help stabilise a portfolio’s overall risk profile. While safe assets tend to offer lower volatility and a higher likelihood of capital preservation, they are not necessarily designed to hedge extreme, short-term market shocks.

The distinction matters because assets that support portfolio stability over time may not always provide protection during periods of acute stress.

This theme has also been explored in a recent Academy session examining how traditional safe havens behave across different types of market stress.

Is gold still a reliable safe haven during market crises?

Gold has long been valued as a store of wealth, from ancient societies to its use as currency before the gold standard was discarded. Has this history contributed to its reputation as a reliable safe haven?

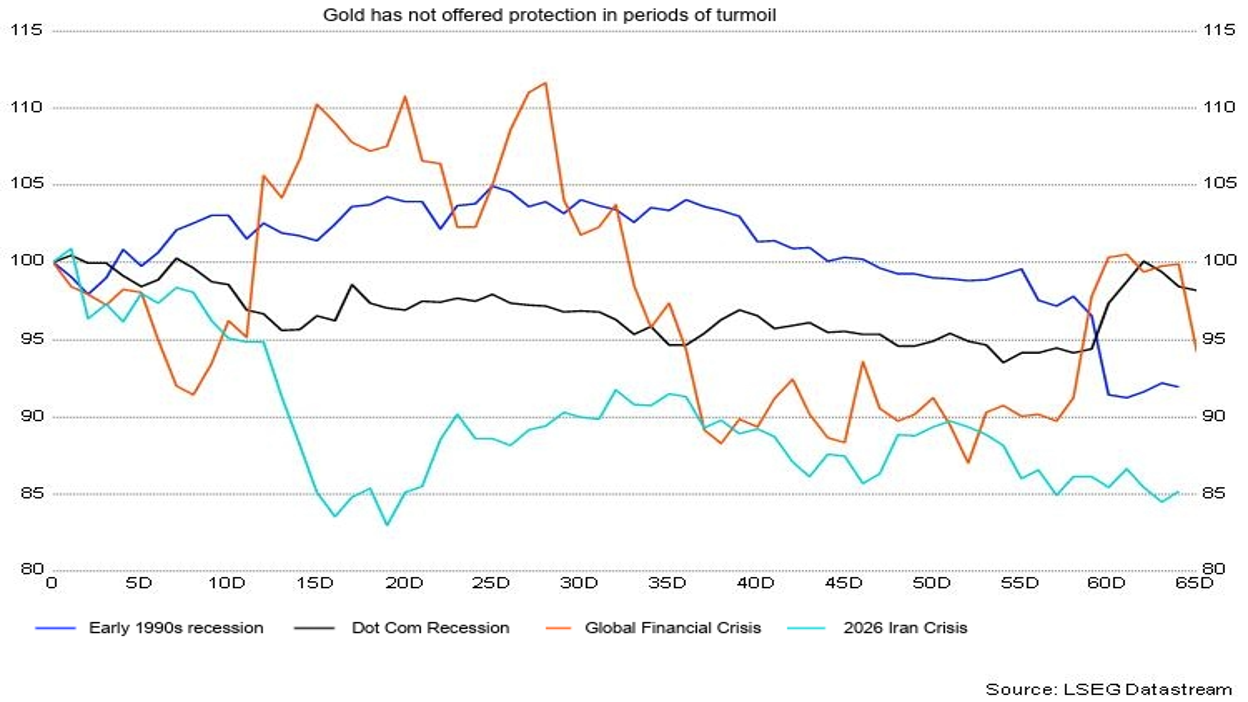

In the below chart, we can see an illustrative comparison based on selected historical episodes over a three-month window, including the early 1990s recession, the dotcom bust, the Global Financial Crisis, and a recent geopolitical event. In each case, gold has not always delivered positive returns. It is also worth noting that short-term performance after a crisis may differ from gold’s longer-term role as an inflation hedge.

The chart indicates that gold’s behaviour in the current market environment differs from its pattern in earlier crises. Two separate factors may help explain this. First, the current shock may differ from earlier financial or market‑driven crises: it has been shaped more by geopolitical conflict and energy‑related inflation. Second, gold prices entered this episode after a sustained, momentum-driven rally that ran until Q1 2026. This suggests that pre-existing investor positioning and subsequent profit‑taking may contribute to differences in short-term performance.

When does the US dollar behave like a safe haven?

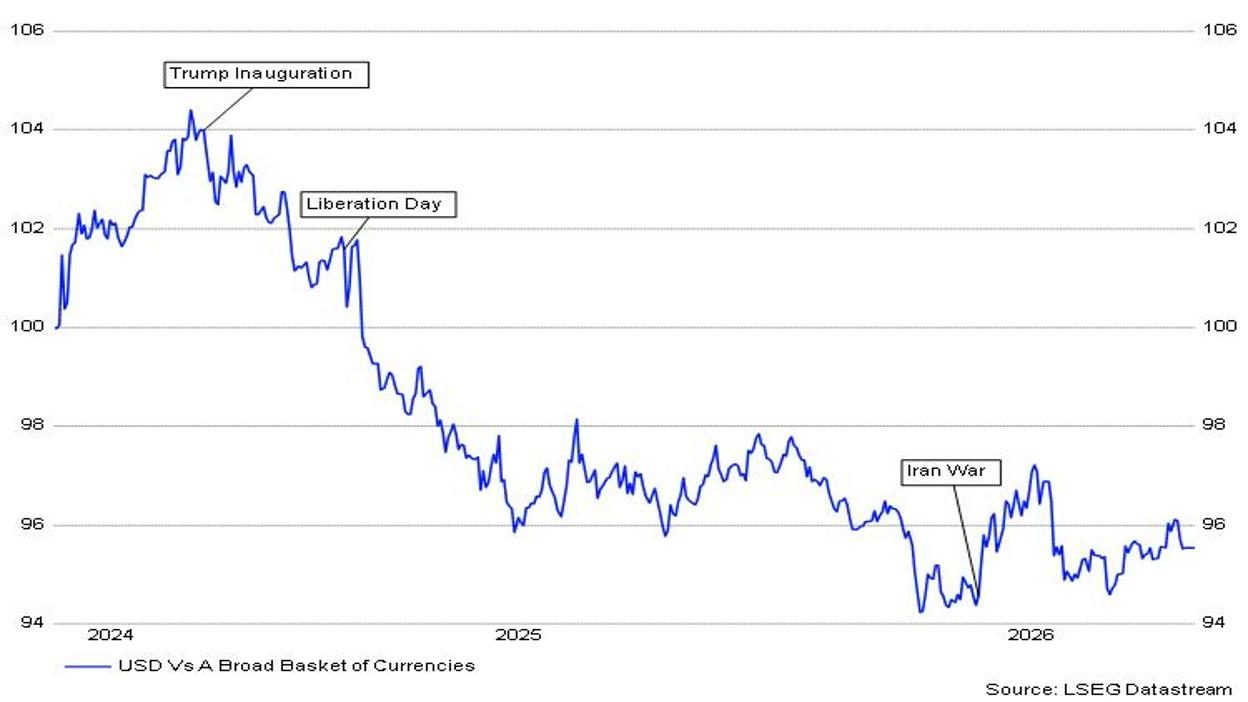

The US dollar has been the world’s dominant reserve currency since the Bretton Woods agreement of 1944 and has historically tended to appreciate during periods of global stress, supported by demand for liquidity.

Recent market behaviour highlights that the dollar’s safe haven role can depend on the underlying drivers of a crisis. From early 2025, increased uncertainty around US trade and economic policy, alongside concerns about the fiscal outlook, coincided with a period of dollar weakness. By contrast, after a recent period of heightened geopolitical tension, the dollar exhibited behaviour more consistent with historical safe haven patterns during a period associated with increased demand for liquidity and changes in energy market conditions.

These contrasting episodes underline that the dollar’s performance may be influenced not only by risk aversion, but also by whether a crisis is primarily financial, fiscal, or geopolitical in nature.

Are US Treasuries a safe haven or a safe asset?

Government-issued securities, such as U.S. Treasuries, are generally considered low-risk due to the strong creditworthiness of the issuer. As a result, this safe haven is commonly viewed as a safe asset.

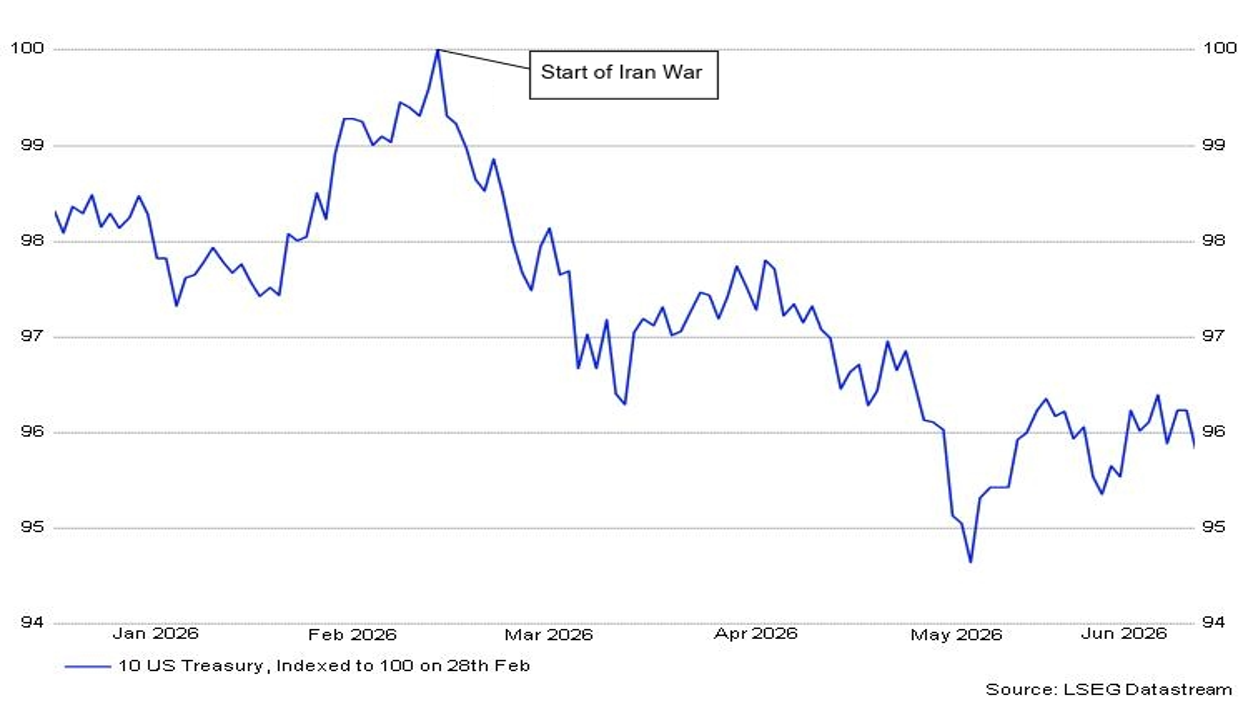

However, 2026 data suggest that safe assets do not necessarily function as safe havens in all market conditions.

Recent observations suggest that Treasury yields have been influenced by evolving market conditions over this period. However, US public finances were already subject to fiscal pressures before any additional defence spending associated with the current environment. Publicly available data suggest that fiscal pressures remain a consideration alongside elevated debt level.

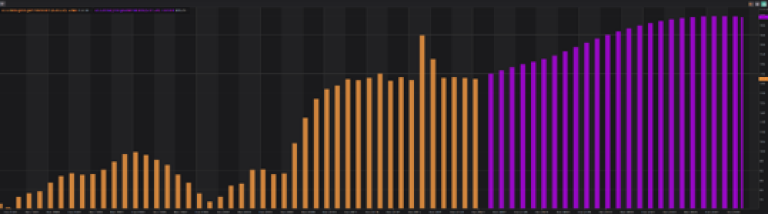

The chart below shows that the US debt as a share of GDP has increased significantly in recent years and is projected to rise further over the longer term.

Source: Economic Indicator App in LSEG Workspace

Higher inflation expectations may lead markets to anticipate potential increases in interest rates, applying upward pressure on Treasury yields. A useful way to monitor market expectations for Federal Reserve policy is through the Interest Rate Probability App (IRPR) in LSEG Workspace. IRPR displays the probabilities and expected change of central bank rates, implied from the market prices of interest rate derivatives.

Higher government spending in a constrained fiscal environment, alongside energy supply risks and rising inflation expectations, may contribute to movements in government bond prices. U.S. Treasuries can be influenced by these broader market dynamics.

Key takeaways for market practitioners

- Safe havens and safe assets are not the same and may require separate evaluation criteria.

- The nature of a crisis matters when assessing asset behaviour.

- Data‑driven analysis is essential when historical relationships no longer hold.

Learn more

To explore how data and analytics available in LSEG Workspace can be used effectively, you may refer to the content available in the Learning Centre. This question around safe haven behaviour was picked up in a recent Markets Unpacked discussion with Reuters.

One way markets price expectations for central bank interest rates is through the pricing of interest rate derivatives, from which market‑implied interest rate probabilities can be inferred and reflected in tools such as the Interest Rate Probability app (IRPR). These dynamics are also explored in a short video walkthrough, while related learning sessions on macroeconomic indicators and interest rate probabilities look at how this analysis is applied.

Disclaimer: This content is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. Past performance and historical observations may not be indicative of future results.

Legal Disclaimer

Republication or redistribution of LSE Group content is prohibited without our prior written consent.

The content of this publication is for informational purposes only and has no legal effect, does not form part of any contract, does not, and does not seek to constitute advice of any nature and no reliance should be placed upon statements contained herein. Whilst reasonable efforts have been taken to ensure that the contents of this publication are accurate and reliable, LSE Group does not guarantee that this document is free from errors or omissions; therefore, you may not rely upon the content of this document under any circumstances and you should seek your own independent legal, investment, tax and other advice. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon.

Copyright © 2026 London Stock Exchange Group. All rights reserved.

The content of this publication is provided by London Stock Exchange Group plc, its applicable group undertakings and/or its affiliates or licensors (the “LSE Group” or “We”) exclusively.

Neither We nor our affiliates guarantee the accuracy of or endorse the views or opinions given by any third party content provider, advertiser, sponsor or other user. We may link to, reference, or promote websites, applications and/or services from third parties. You agree that We are not responsible for, and do not control such non-LSE Group websites, applications or services.

The content of this publication is for informational purposes only. All information and data contained in this publication is obtained by LSE Group from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data are provided "as is" without warranty of any kind. You understand and agree that this publication does not, and does not seek to, constitute advice of any nature. You may not rely upon the content of this document under any circumstances and should seek your own independent legal, tax or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the publication and its content is at your sole risk.

To the fullest extent permitted by applicable law, LSE Group, expressly disclaims any representation or warranties, express or implied, including, without limitation, any representations or warranties of performance, merchantability, fitness for a particular purpose, accuracy, completeness, reliability and non-infringement. LSE Group, its subsidiaries, its affiliates and their respective shareholders, directors, officers employees, agents, advertisers, content providers and licensors (collectively referred to as the “LSE Group Parties”) disclaim all responsibility for any loss, liability or damage of any kind resulting from or related to access, use or the unavailability of the publication (or any part of it); and none of the LSE Group Parties will be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, howsoever arising, even if any member of the LSE Group Parties are advised in advance of the possibility of such damages or could have foreseen any such damages arising or resulting from the use of, or inability to use, the information contained in the publication. For the avoidance of doubt, the LSE Group Parties shall have no liability for any losses, claims, demands, actions, proceedings, damages, costs or expenses arising out of, or in any way connected with, the information contained in this document.

LSE Group is the owner of various intellectual property rights ("IPR”), including but not limited to, numerous trademarks that are used to identify, advertise, and promote LSE Group products, services and activities. Nothing contained herein should be construed as granting any licence or right to use any of the trademarks or any other LSE Group IPR for any purpose whatsoever without the written permission or applicable licence terms.