Anubhuti David

The payments industry continues to evolve and grow at pace, delivering speed, efficiency and opportunity for global stakeholders. At the same time, the risk landscape is changing – and industry players need to ensure that they keep well-informed of emerging risks. Let’s look at some key trends we anticipate in the payments space as the new year unfolds.

- As digital transformation of the financial ecosystem continues, explore the new opportunities and risks that are emerging for the payments industry.

- Discover the 5 predicted risk trends for the payments space, and how to manage a complex risk landscape.

Opportunity and risk: hand-in-hand

As the digital transformation of the financial ecosystem continues apace, new opportunities and new risks are emerging. The payments industry in particular is evolving at speed – and alongside this evolution, risk stakes are rising.

The payments industry is key to the digital financial ecosystem. It delivers speed, efficiency and 24/7 connectivity to individuals, businesses and banks, helps to smooth global payments and transactions, keeps the pace of business swift, and more. At the same time, however, accelerating digitalisation and rapid growth within the payments space has meant that financial criminals have increasingly targeted the industry, which has seen an uptick in criminal activity – ranging from account takeovers and customer deception, to money laundering and more.

Given growing financial crime rates, players in the payments space need to remain vigilant when it comes to identifying potential risk and complying with international regulations, especially given that regulatory fines are rising.

In 2023, total penalties for failing to comply with regulations amounted to US$6.6 billion, a significant increase from US$4.2 billion in 2022. Many of these fines were issued against crypto and payments firms – accounting for 69% and 21% of global penalties respectively.

Global financial institution AML and regulatory fines soar in 2023 (fenergo.com)

Looking ahead, we expect to see growth in the digital and contactless payments area – including mobile wallets and contactless cards – and we further anticipate a continued rise in cryptocurrency transactions as crypto and digital assets continue to gain more mainstream acceptance. Payments innovations will continue and we expect ongoing expansion in the payments options available on e-commerce platforms, for example BNPL (Buy Now Pay Later). We also expect to see stronger security measures as firms focus on fraud detection technology, as well as AI- and ML-based solutions to help prevent unauthorised transactions.

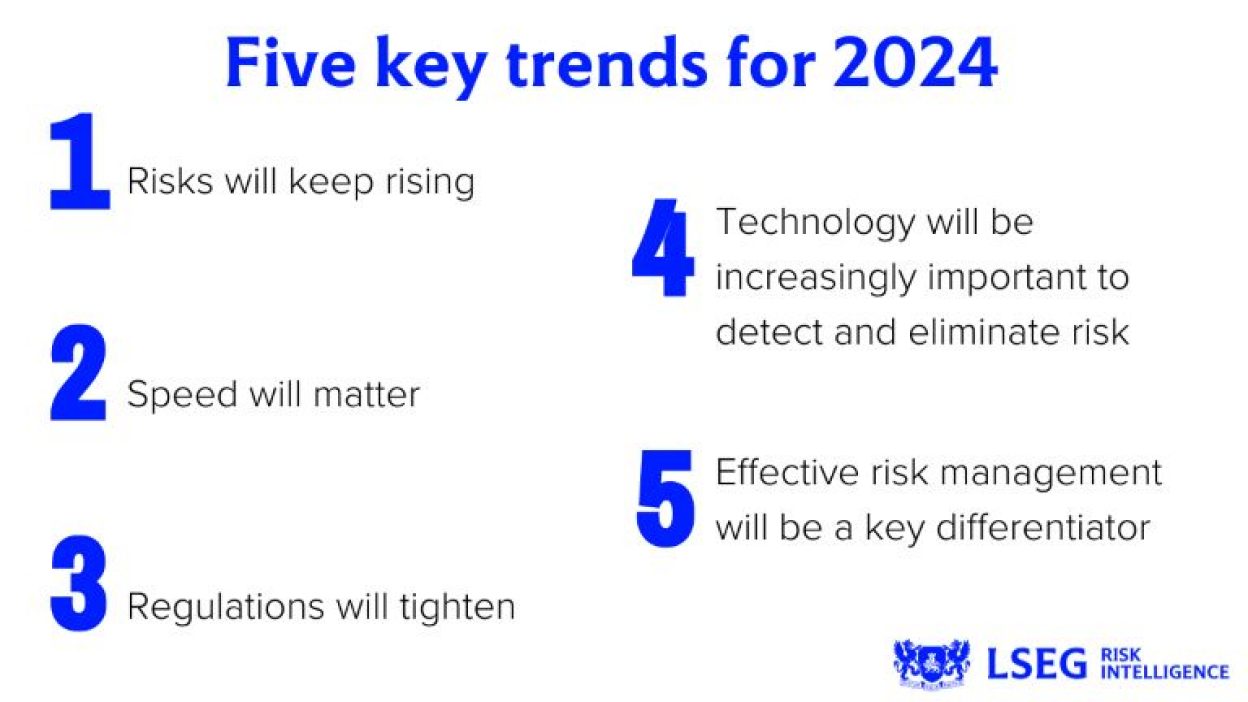

Against this broad backdrop, here are our top five key trends to watch in 2024:

Risk will keep rising

Sophisticated criminal activity will continue to drive risk levels across the payments space, and we expect risk to keep rising into 2024 and beyond. Financial criminals are ever-more adept at leveraging new technology to commit fraud and other forms of financial crime and this means that payments companies need to ensure that they remain one step ahead of such activity at all times.

PwC’s Global Economic Crime and Fraud Survey 2022 reveals an example of this, highlighting that as our collective global use of platforms has risen exponentially in recent years, so too has platform-related fraud. The survey found that this type of fraud is at alarming levels, with a substantial 40% of organisations encountering fraud experiencing platform fraud. Interestingly, fraudulent transfers to or from a platform topped the list of the most common type of platform fraud[1].

Speed will matter

Speed will remain crucial. Customers expect quick, seamless online experiences that do not slow the pace of business. They value speed and efficiency, and this means that organisations should focus on, for example, accelerating their instant payment adoption and their ability to verify payments in real time. All processes need to be as low-friction as possible to prevent customer abandonment rates from rising.

In support of this point, a 2023 Citi survey – the “Future of Payments Survey” – found that speed is a key consideration for many clients. The organisation gathered insights from over 100 of their financial institution clients and found that speed is one of the biggest pain points for bank clients, second only to cost concerns[2].

Regulations will tighten

Global regulations have been tightening, and this trend shows no sign of abating in 2024. Regulators are expected to be particularly active across newer, high risk industries – with examples including BNPL, crypto, casinos, gaming and online betting, and more.

Examples of relevant legislation include:

- Across the EU, the Payment Services Directive (PSD2), Markets in Crypto-Assets Regulation (MiCA) and the 5th Anti-Money Laundering Directive (5AMLD) are in force. EU legislators are currently working on a proposal to amend and modernise the current Payment Services Directive (PSD2) which will become PSD3 and establish, in addition, a Payment Services Regulation (PSR). Work is also underway on a new legislative proposal on financial data access (FIDA) and on reviewing EU AML legislation (the AML Package).

- In India there is a focus strengthening the regulatory framework o for authorised dealer banks and payments aggregators and their need to comply with cross border payments regulations. In 2023, The Reserve Bank of India issued guidelines to regulate entities “facilitating cross border payment transactions for import and export of permissible goods and services in online mode”.

- In the US, Fednow is an instant payments service developed by the Federal Reserve Bank (Fed). It was launched in July 2023 as a “soft regulation”[4], and we expect wider adoption next year.

Firms should also remain acutely aware of the sanctions landscape, which has become increasingly complex in the wake of the Russia-Ukraine conflict.

Fully understanding the regulatory landscape is essential to remaining compliant, especially as we expect to see increased regulatory scrutiny and a potential rise in fines issued this year. We recommend implementing a risk-based approach, regularly updating sanctions lists and databases, and investing in employee training.

Technology will be increasingly important to detect and eliminate risk

The range of demands on the payments industry, including complying with evolving regulations and ensuring smooth customer processes, can be met by carefully choosing the right technology: screening and compliance processes need to be both fast and accurate.

Many firms also face rising cost pressures, but the efficient use of technology can help to ease this financial pressure. For example, for Payment Service Providers (PSPs), omnichannel solutions and API technology in particular can offer cost-effective, speedy solutions across geographies.

Effective risk management will be a key differentiator

Those companies that successfully leverage technology in the payments space and implement effective risk management strategies can use this to build a very real competitive advantage.

Technology can help companies manage a range of priorities, including identifying and preventing fraud and other forms of financial crime, meeting regulatory obligations and delivering a positive customer experience.

This means that there could be a need for some hands-on transformation within risk management teams – processes may need to be adapted to support the use of new technology – but any such changes are likely to deliver positive results: it is safe to say that effective risk management can play a key role in differentiating one offering from another.

Managing a complex risk landscape

As companies strive to manage a complex 2024 risk landscape – across the payments space and beyond – many may choose to partner with specialists that are able to deliver the technology needed to effectively manage risk, meet compliance obligations and deliver seamless, low-friction customer experiences.

When selecting solutions, compliance teams should look for end-to-end risk management and tools that span screening, due diligence, identity verification, account verification and digital onboarding, since these elements are all essential to developing a comprehensive risk management strategy.

As the new year unfolds, identifying, managing and mitigating risk needs to remain high on the agenda as companies work to remain compliant with global regulations, while focussing on maximising the many opportunities presented by ongoing digitalisation.

1. https://www.pwc.com/gx/en/services/forensics/economic-crime-survey.html

2. https://www.citigroup.com/global/insights/treasury-and-trade-solutions/future-of-payments-survey

3 https://www.aciworldwide.com/fednow?utm_source=google&utm_medium=cpc&utm_campaign=pm-2023-bnks-rtpy-all-global-inside-real-time-google-paid-pdad&adgroup=&utm_term=fednow&utm_content=670956581448&gad_source=1&gclid=CjwKCAiAvJarBhA1EiwAGgZl0D3P3Zh40FnY3mpLMcC6_ssdoJzztmUhHO_qMARgUSr3PalBfuAuRRoC4LgQAvD_BwE

Legal Disclaimer

Republication or redistribution of LSE Group content is prohibited without our prior written consent.

The content of this publication is for informational purposes only and has no legal effect, does not form part of any contract, does not, and does not seek to constitute advice of any nature and no reliance should be placed upon statements contained herein. Whilst reasonable efforts have been taken to ensure that the contents of this publication are accurate and reliable, LSE Group does not guarantee that this document is free from errors or omissions; therefore, you may not rely upon the content of this document under any circumstances and you should seek your own independent legal, investment, tax and other advice. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon.

Copyright © 2024 London Stock Exchange Group. All rights reserved.

The content of this publication is provided by London Stock Exchange Group plc, its applicable group undertakings and/or its affiliates or licensors (the “LSE Group” or “We”) exclusively.

Neither We nor our affiliates guarantee the accuracy of or endorse the views or opinions given by any third party content provider, advertiser, sponsor or other user. We may link to, reference, or promote websites, applications and/or services from third parties. You agree that We are not responsible for, and do not control such non-LSE Group websites, applications or services.

The content of this publication is for informational purposes only. All information and data contained in this publication is obtained by LSE Group from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data are provided "as is" without warranty of any kind. You understand and agree that this publication does not, and does not seek to, constitute advice of any nature. You may not rely upon the content of this document under any circumstances and should seek your own independent legal, tax or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the publication and its content is at your sole risk.

To the fullest extent permitted by applicable law, LSE Group, expressly disclaims any representation or warranties, express or implied, including, without limitation, any representations or warranties of performance, merchantability, fitness for a particular purpose, accuracy, completeness, reliability and non-infringement. LSE Group, its subsidiaries, its affiliates and their respective shareholders, directors, officers employees, agents, advertisers, content providers and licensors (collectively referred to as the “LSE Group Parties”) disclaim all responsibility for any loss, liability or damage of any kind resulting from or related to access, use or the unavailability of the publication (or any part of it); and none of the LSE Group Parties will be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, howsoever arising, even if any member of the LSE Group Parties are advised in advance of the possibility of such damages or could have foreseen any such damages arising or resulting from the use of, or inability to use, the information contained in the publication. For the avoidance of doubt, the LSE Group Parties shall have no liability for any losses, claims, demands, actions, proceedings, damages, costs or expenses arising out of, or in any way connected with, the information contained in this document.

LSE Group is the owner of various intellectual property rights ("IPR”), including but not limited to, numerous trademarks that are used to identify, advertise, and promote LSE Group products, services and activities. Nothing contained herein should be construed as granting any licence or right to use any of the trademarks or any other LSE Group IPR for any purpose whatsoever without the written permission or applicable licence terms.